By Nicole Ayo von Thun, Senior Advisor, International Engagement; and Matt Chan, Director, Data and Analytics, Office of the Auditor-General in New Zealand

Supreme Audit Institutions (SAIs) are operating in an increasingly digital environment. COVID-19 has sped up the adoption of digital technologies by several years and it is expected that these changes are here to stay. Keeping up-to-date with the digital transformation of the workforce is important for SAIs to continue to add value and remain relevant.

Throughout the year PASAI has shared blogs on the topics of online collaboration, building digital resilience and cyber security. Adding to this digital theme, this blog looks at the benefits for a SAI in building digital literacy. Digital literacy is the knowledge and ability to use computers and related technology efficiently and effectively. In the past, digital literacy may not have been apriority for your SAI, however COVID-19 has increased the urgency for all SAIs to focus more on this issue. COVID-19 has prompted many SAIs to reconsider their competencies and make some strategic shifts to the way they work. Has your SAI assessed its current strengths and weaknesses in digital competency and literacy?

Digital literacy is not about investing in massive technological platforms or even becoming technology experts. It is about equipping auditors with the digital skills, tools and key competencies required to audit in an environment that is increasingly reliant on technology and where large amounts of data are generated. Auditors need to understand how to harness the power of Data Analytics, Big Data, and Artificial Intelligence to audit more efficiently and effectively – using them as tools to capture, verify and track transactions using large data sets, with lower cost (in some instances) and limited human intervention.

An understanding of data governance and management is also required and is key to effectively manage data as one of our most valuable assets. This area includes the development of a data governance framework, policies and procedures, and will be covered in greater detail in a forthcoming blog.

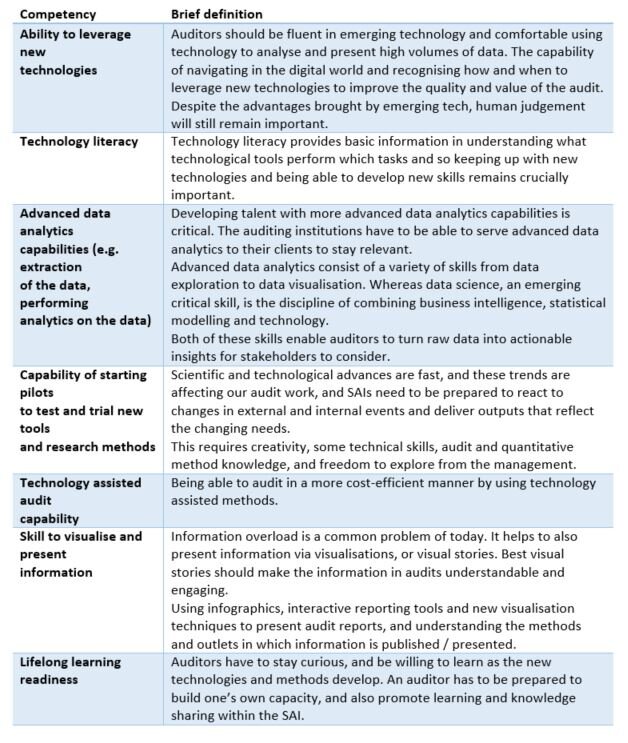

A recent INTOSAI Capacity Building Committee Occasional Paper on The future-relevant and value-adding auditor[1] outlines competencies that auditors require to build digital literacy. The Paper recommends that to build digital literacy SAIs must embrace new technologies to remain ‘future-relevant and value-adding’, even if these new technologies seem daunting. Increasing digital literacy can be achieved by both the SAI as a whole and their individual staff members by working towards some critical competencies. The CBC paper sets out seven competencies and these are presented below:

More information on the recent INTOSAI Capacity Building Committee Occasional Paper on The future-relevant and value-adding auditor can be found here. The Paper provides more detail on 3 other competency areas that SAIs need to focus on in order to remain future-relevant and value-adding: https://www.intosaicbc.org/wp-content/uploads/2020/11/20201106-The-Future-Relevant-Value-Adding-Auditor_CBC_Nov-2020.pdf

What’s next

Stay tuned to read more about the following topics upcoming in our blog series:

SAI Independence

Managing staff productivity and well-being.

Data governance and data management.

We welcome your feedback and look forward to hearing about other priority topic areas of interest to you. Please email: secretariat@pasai.org

[1] INTOSAI Capacity Building Committee (2020, November 6). Occasional paper on the future-relevant value-adding auditor. https://www.intosaicbc.org/wp-content/uploads/2020/11/20201106-The-Future-Relevant-Value-Adding-Auditor_CBC_Nov-2020.pdf.

The Pacific Association of Supreme Audit Institutions (PASAI) is the official association of supreme audit institutions (SAIs) in the Pacific region, and a regional organisation of INTOSAI and promotes transparent, accountable, effective and efficient use of public sector resources in the Pacific. It contributes to that goal by helping its member SAIs improve the quality of public sector auditing in the Pacific to recognised high standards. Due to the global coronavirus pandemic (COVID19), this has restricted PASAI’s delivery of our programs to our Pacific members and in lieu of this PASAI will be providing a series of blogs on various topics that may help auditors think about some implications to service delivery as a result of COVID19.

For more information about PASAI refer www.pasai.org